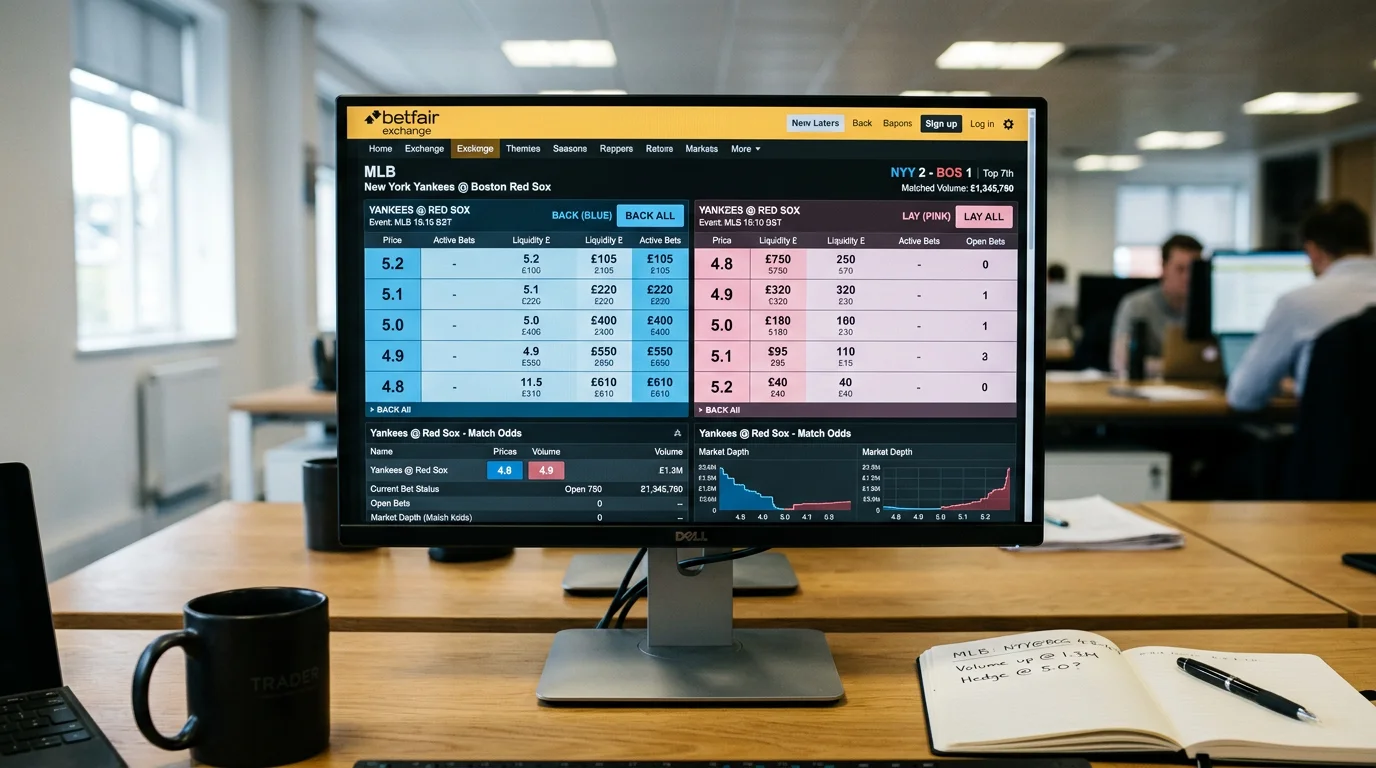

The first MLB lay bet I ever placed was against the Dodgers at 1.41 in May. Seven years on, the screen still feels familiar – two columns of prices, the blue back side, the pink lay side, a depth bar showing how much money is queued at each rung of the ladder. The Betfair Exchange is the only mainstream UK platform where I can take the role of the bookmaker on a baseball market, set my own odds and wait for someone to match me. That capacity unlocks a category of plays that are simply unavailable on a fixed-odds shopfront. The trade off is unfamiliarity, and for a UK punter raised on the high-street betslip, the Exchange’s mechanics take real practice. This piece walks through how lay betting actually works on MLB, where the edges live and where the traps sit.

The Exchange Model Versus a Traditional Sportsbook

Years ago I tried to explain the Exchange to a friend over a pint and watched his eyes glaze. The trick is to drop the financial language and use the right mental picture. A fixed-odds bookmaker is a shop selling priced products. The Exchange is a marketplace where customers trade with each other, and Betfair is the venue host that takes a cut.

The structural difference matters in numbers. The UK remote betting market produced £2.6 billion in gross gambling yield in the most recent fiscal year, and that revenue includes both fixed-odds operators paying out from their book and exchange platforms taking a commission on net winnings. The Exchange does not run a margin in the bookmaker sense. It pairs a back bet at a given price against a lay bet at the same price, holds both stakes in escrow, and at settlement releases winnings minus a commission. The implied margin on an Exchange market is therefore close to zero – sometimes the prices on offer beat the best fixed-odds shops by ten or fifteen pence on a Yankees moneyline, sometimes they do not. The variance is liquidity-driven, not house-rule-driven.

The other operational difference is execution risk. A fixed-odds bookmaker honours the price you click at. The Exchange honours the price someone matches you at. If you click 2.10 and only 2.04 is on offer, you either wait for 2.10 to be matched – which may never happen – or you accept the partial match at 2.04 and re-queue the rest.

How a Lay Bet on an MLB Team Actually Works

The first time a punter lays an MLB team and sees the liability calculation pop up, the maths can shock. Backing the Phillies at 4.0 stakes whatever you choose to put on. Laying the Phillies at 4.0 commits you to paying out three times the stake you accept from the other side. The Exchange’s risk model makes the asymmetry obvious in red type, and it is the single most common reason new exchange punters mis-size a position.

Pick a worked example. I want to lay the Cubs at 2.20 against the Pirates with a backer’s stake of £20 – meaning I am willing to play the bookmaker’s role and accept £20 from someone who wants to back Chicago at 2.20. If the Cubs win, I owe the backer £24 in winnings; my liability is £24, the backer’s stake of £20 stays with them as their winning return on top. If the Cubs lose, I keep their £20. The risk-reward is the same as setting a moneyline price, just from the opposite side of the market. For a fuller treatment of how moneyline pricing works in fixed-odds form, the explainer walks through the backer’s view of exactly the same question.

The reason lay betting becomes useful in baseball is the underlying volatility of the sport. Roughly thirty per cent of all MLB games are decided by a single run, which means a 2.20 favourite is rarely a 2.20 favourite in any clean probabilistic sense – the price absorbs the pitcher matchup, the bullpen state and a heavy dose of unhedged variance. Laying short-priced MLB favourites in matchups where the pitching gap is narrower than the price implies is a classic Exchange play, and the Exchange is the only mainstream UK venue that pays you to take that view.

Commission and What You Actually Take Home

The single most misunderstood part of the Exchange is commission. New users assume it is charged on stake. It is not. It is charged on net market winnings, paid only on the side you finished in profit on across the relevant market.

The standard UK commission rate sits in the five per cent band, and it tapers down for high-volume customers via a points-based system. On a £100 net win, you keep £95. On a £100 net loss, you pay nothing extra. There is no commission on the gross – only on the win. That structural detail is what makes the Exchange viable as a trading venue, because it lets you place dozens of small bets without bleeding to a per-trade fee.

The legal and regulatory backdrop is shifting. Stephen Piepgrass, a partner at the gaming-law firm Troutman Pepper Locke, summed it up in plain terms when he said we are likely to see more calls for regulation in this space. He was talking about the wider US betting market, but the principle applies on this side of the Atlantic. The Exchange operates inside the UK regulatory perimeter, with the same KYC, AML and advertising rules as the fixed-odds shops, and the small additions on the horizon – micro-bet caps, prop-level integrity rules – will catch the Exchange too. Commission will probably stay where it is, because that is the platform’s structural revenue line. The auxiliary rules are the moving parts.

Liquidity on MLB Exchange Markets

The Exchange’s biggest weakness on baseball is liquidity. UK volumes on MLB are a fraction of UK volumes on Premier League football, and that gap shows up as thinner depth on the price ladder, wider gaps between back and lay, and slower fills on bigger stakes.

For a marquee MLB game during peak UK evening hours, the moneyline ladder typically holds £30,000 to £80,000 of matched volume across the day, and headline run-line and total markets clear similar volumes. For a Tuesday matinee at Coors Field, the moneyline matched volume might be a tenth of that, and any stake above £200 will move the price visibly. A £1,000 lay on a Marlins moneyline at three in the morning UK time is unlikely to get filled at the price you want.

The fix is patience. Place your lay at the price you actually want, queue it, and walk away. The match either comes or it does not. Chasing the line by repeatedly inching the price down is the fastest way to underprice your own book on a market that was already thin.

Trading Run-Lines in Play

In-play run-line trading on the Exchange is a discipline of its own – you back at one price, lay at a shorter price as the game moves, and pocket the difference regardless of the final result. The mechanic is identical to financial market trading, and the rhythm of MLB makes it work. Pick a side at +1.5 in the second inning, let the game develop, and lay the same side at +1.5 in the seventh if a swing in the score has shortened the price. The discipline is exit timing. Run-line markets often whipsaw on a single half-inning, and the temptation to chase a position through the eighth is what costs experienced traders the most.

Where the Exchange Fits in a UK Punter’s Toolkit

The Betfair Exchange is not a substitute for a fixed-odds sportsbook. It is a complementary venue for a specific category of MLB plays – laying short favourites, pricing your own back odds on niche markets, in-play run-line trading, and hedging futures positions late in a season. The learning curve is steeper than on a fixed-odds platform, the liquidity is shallower, and the commission compounds quietly across heavy trading. The reward is the ability to take positions a fixed-odds book will never let you take. For an MLB analyst working volume, that capacity is worth the friction. For a casual UK punter who places ten bets a season, the Exchange is probably an unnecessary complication.

Why do Betfair Exchange MLB markets go thin between innings?

Does Betfair's commission make MLB lay betting unprofitable for small stakes?

Material created by the team StitchLine